GridGain powers instant, always-on payments

Deliver faster, more reliable, and more secure payment services with the GridGain unified real-time data platform.

Why the Payments industry needs modernization

Demand for faster payments is soaring from digital wallets to account-to-account (A2A) transfers and cross-border transactions. Financial institutions must deliver secure, scalable systems that handle massive transaction volumes with ultra-low latency without re-architecting core systems.

How GridGain solves the Payments industry challenges

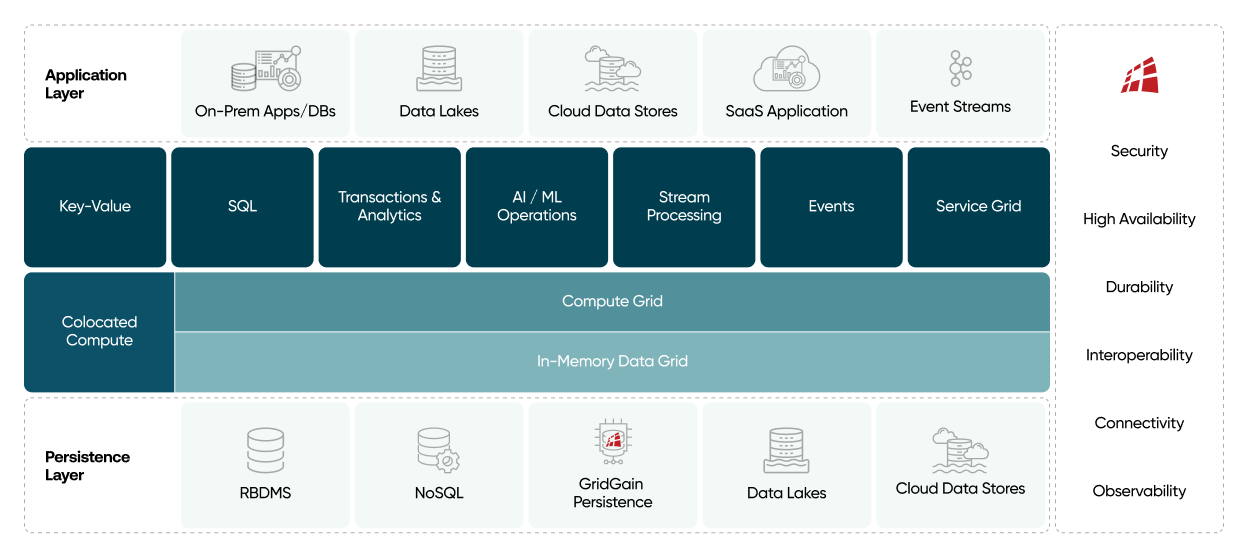

GridGain combines in-memory speed, persistent storage, and distributed compute in a unified real-time data platform.

The result: massive scalability, transaction consistency, high availability with near-zero RTO, and up to 10x faster performance.

Problems that the GridGain unified real-time data platform solves:

GridGain payment services use cases

Digital wallets and real-time payments (RTP) are now core to modern payments, but most banking and PSP architectures weren’t built for always-on, instant transactions.

GridGain: Enabling fast, always-on digital wallets

GridGain provides an ultra-low-latency data layer for digital wallets and RTP, offering in-memory processing for real-time checks (balance, risk, KYC/AML), horizontal scalability for peak bursts, and a distributed, fault-tolerant design and near-zero RTO for 24/7 uptime.

It delivers transactional consistency for instant ledger updates, enables unification of fragmented data for millisecond decisioning, and includes encryption/RBAC/audit trails to meet regulatory needs enabling responsive, scalable, always-available digital wallet experiences without re-architecting core systems.

Without a scalable, performant, and reliable data layer, A2A growth means higher risk, higher cost, and degraded customer experience.

GridGain: Powering real-time A2A at scale

GridGain enables banks and FinTechs to deliver instant, reliable A2A payment services with an architecturally superior data platform that unifies in-memory speed, persistent storage, and distributed compute in one integrated system.

In-memory processing provides real-time access for balance checks, fraud detection, and approvals, while being a horizontally scalable, fault-tolerant architecture and near-zero RTO, with transactional consistency, supporting millions of transfers with millisecond latency and no downtime.

Built-in encryption, RBAC, and ML-powered fraud detection meet compliance needs, and GridGain simplifies adding RTP, FedNow, and Open Banking services without requiring you to re-architect your core systems.

Read the blog post to learn more: Supporting Instant Account-to-Account Transfers at Scale

Cross-border payments are growing rapidly as businesses and consumers demand faster, cheaper, and more transparent international transfers.

Powering real-time cross-border payments

GridGain helps banks and PSPs deliver faster, more transparent cross-border payments with an architecturally superior data platform that provides in-memory speed, persistent storage, and distributed compute in one integrated system. Its unified real-time data platform gives instant access to payment, FX, and compliance data for routing, screening, and fraud detection at millisecond speed. The GridGain platform scales to handle millions of transactions while maintaining transactional consistency and predictable latency. A distributed, fault-tolerant architecture and near-zero RTO ensure 24×7 uptime, while built-in security and audit trails support compliance. With GridGain, institutions can cut processing costs, reduce exceptions, and add new corridors or ISO 20022 messaging capabilities without re-architecting their core systems.

Read the blog post to learn more: Supporting Cross-Border Payments at Scale

Customer Success

Financial analytics company accelerates fraud processing 10X with GridGain

Multinational Banking Corporation Accelerates Digital Transformation with GridGain

Featured Resources