Connecting to an A2A rail is the easy part. The harder job is running pay-by-bank flows in real time: fraud checks, routing, reconciliation, and failover, all without ripping out the core systems already in place.

Account-to-account payments are expanding fast across SEPA Instant, FedNow, RTP, and UPI. Banks, PSPs, and infrastructure teams see the appeal: quicker settlement, fewer intermediaries, lower processing costs, and a better customer experience. But growth in A2A also exposes a harder truth. Many organizations are trying to run always-on, account-based payment flows on platforms designed for batch jobs, siloed data, and slow recovery. When that happens, the problem is not only latency. It is operational weakness that shows up at exactly the wrong time.

For payments strategy, modernization, and integration teams, success is not defined by getting onto a new rail. It is defined by what happens after connection: can the system make fraud and routing decisions inside the processing window, hold up under peak volume, recover cleanly from failures, and fit into the existing estate without creating another silo or forcing a core replacement? Those are the questions that decide whether A2A becomes a growth channel or an operational liability.

A2A growth is exposing an operations gap

A2A is not simply one more payment type to support. It pushes teams away from card-centric or deferred-processing models and into a world of direct account movement, instant decisions, and continuous availability. For the people running the payment stack, that makes A2A as much an operational discipline as a product opportunity.

With instant A2A flows, the window to validate, decide, route, and confirm is measured in moments. Fraud checks cannot wait for a downstream batch. Reconciliation cannot be left to overnight clean-up. Recovery cannot rely on guesswork. Whether the payment is a checkout transaction, bill payment, or real-time disbursement, the system has to act on complete, current context while the transaction is still in flight. That is why A2A strains operations as much as it changes payments.

Inside the payments organization, that pressure shows up in the metrics that matter: peak throughput, zero-downtime availability, transaction integrity, fraud decision speed, failover readiness, and clean integration with core banking, Kafka, and long-lived payment systems.

Why batch-era payment systems struggle with A2A payments

Most payment estates were not designed for a streaming environment. They were built for a world in which updates could be staged, latency was tolerable, and failures could be cleaned up later. Pay-by-bank flows do not give teams that cushion.

In many batch-oriented architectures, a single transaction touches multiple systems: one for payment data, another for customer or account context, another for fraud, and another for posting or ledger state. Every hop adds delay. Every silo makes it harder to act on live data. Every dependency increases the chance that one slow or unhealthy service drags down the entire flow. What was acceptable in deferred-processing environments becomes brittle in real time.

The failure patterns are easy to recognize. A deployment corrupts transactions in the middle of the day. A data-center issue slows performance during peak traffic. Fraud models miss the decision window. Volume spikes expose throughput limits. In each case, the real question is not just how fast the system is, but whether it can stay fast, accurate, and recoverable under stress.

Four bottlenecks behind slow or fragile A2A payments

Fragmented operational data

Payment, fraud, compliance, customer, and ledger data often sit in different systems with different latencies and access patterns. That fragmentation slows approvals, complicates routing, and makes reconciliation harder. It also raises the odds that critical decisions are made with stale or partial context.

Decision latency inside the processing window

A2A systems have to validate balances, apply fraud controls, and choose routes quickly enough to stay within rail timing requirements and customer expectations. At scale, even small delays compound quickly.

Failover and recovery risk

In real-time payments, a failure is not only an availability issue. It is a transaction-integrity issue. Teams need confidence that valid transactions remain intact, sites stay in sync, and recovery does not leave behind manual cleanup.

Modernization risk from rip-and-replace thinking

Most institutions know they need a more modern payments architecture. They also know that core replacement is expensive, risky, and hard to execute. In practice, the better path is usually to modernize the operational tier around the core: add real-time capability where it matters most while existing systems continue doing the work they still do well.

What modern A2A payments architecture needs to do

Modern A2A architecture has to do more than conduct transactions fast. It has to keep payments correct when the system is under pressure.

That means running instant validation and fraud checks against live operational data. It means giving routing and reconciliation logic a current view of the transaction instead of making each payment wait on disconnected systems. It means scaling horizontally during spikes without redesigning the platform every time a new rail, market, or use case appears. It means staying available through failures and recovering precisely when something does go wrong. And it means doing all of that alongside core banking systems, mainframes, event backbones, and long-lived payment engines that are not going away anytime soon.

This is where a real-time operational tier matters. It provides a real-time layer where payment, fraud, compliance, and ledger-related context come together for A2A decisioning and execution. That is a better answer than treating account-to-account payments as a simple rail-integration project.

What good looks like in the market

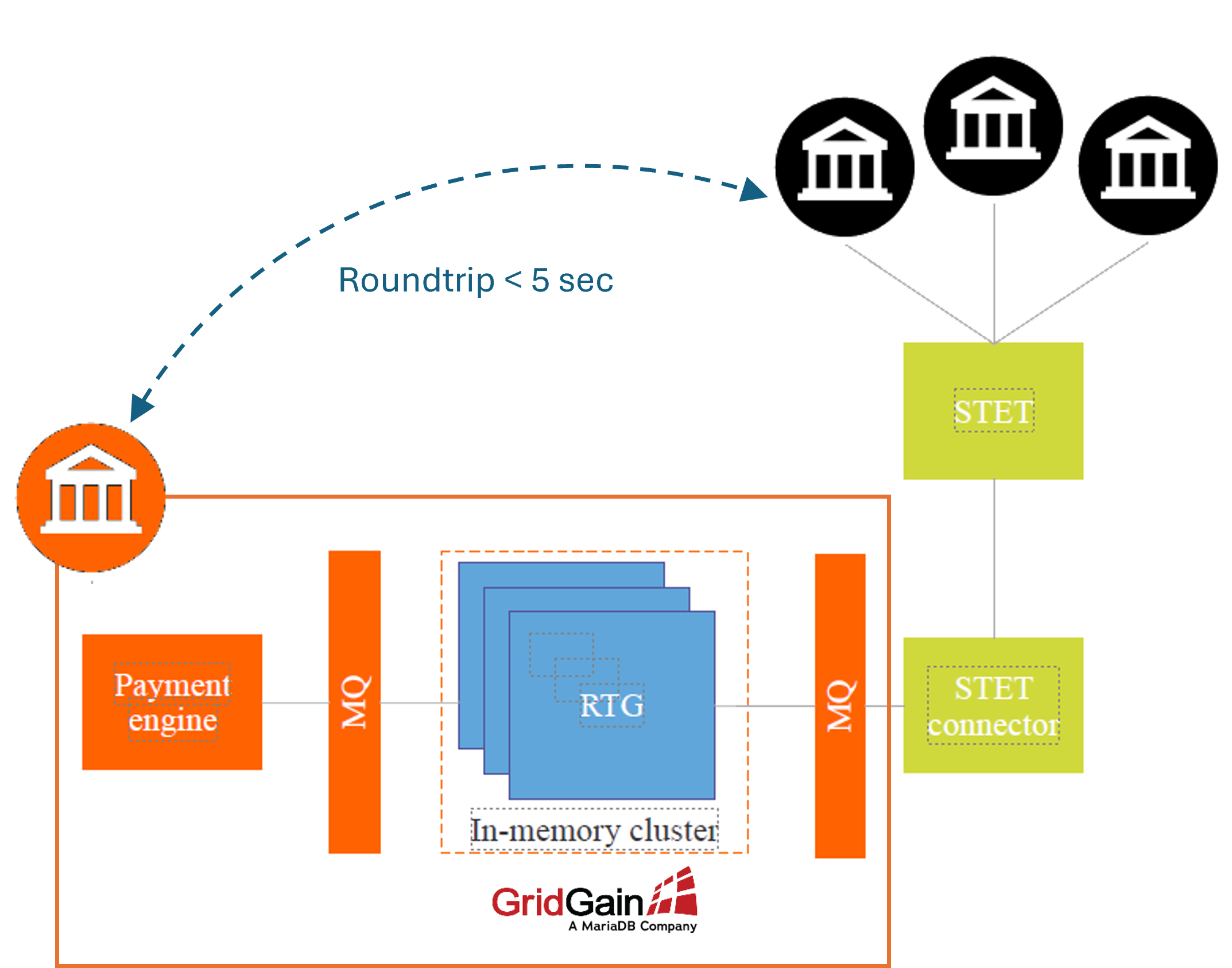

A top global bank offers a clear example of this pattern. In its SEPA Instant Payments Gateway, the bank used GridGain’s in-memory compute platform to connect the STET instant-payments environment to existing mainframe payment systems. The architecture supports ISO-to-COBOL transformation, high-volume message handling, and real-time processing within the timing requirements of instant rails. The bank also used the platform to offload mainframe demand, handle large transaction volumes, and expose payment-related data through APIs without replacing core systems.

Figure 1: Top Global Bank Real-time Gateway (RTG)

In most payment environments, modernization does not begin with a greenfield stack. It begins with a real-time operational tier that can support modern A2A requirements, speed up decisioning, and absorb new load while existing systems remain in place.

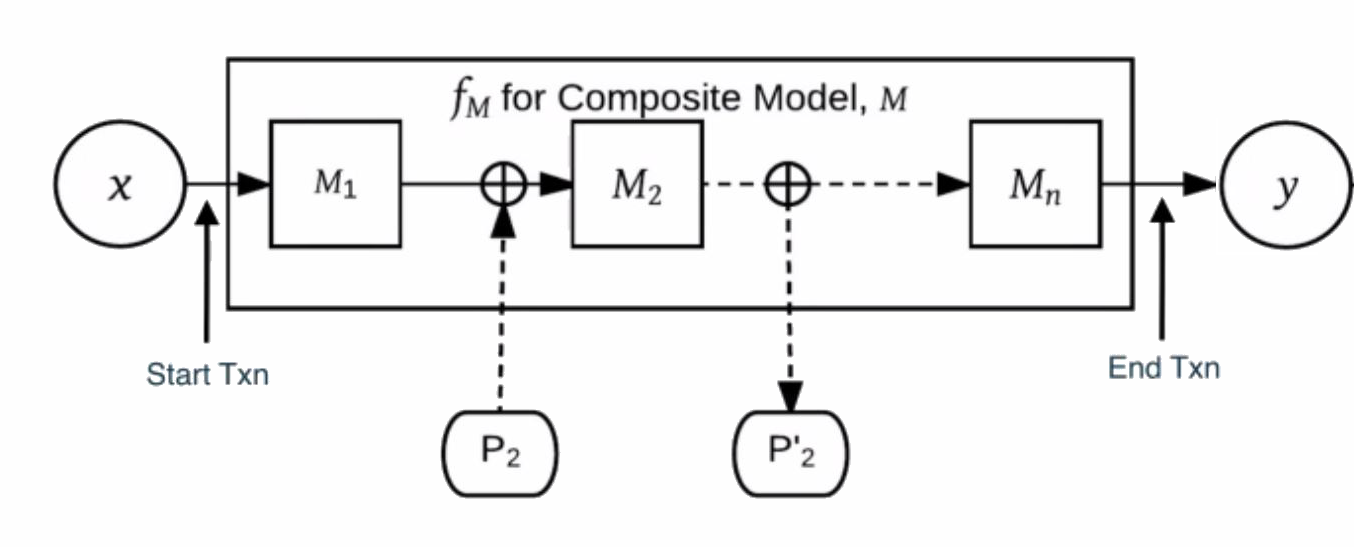

A leading financial analytics software company highlights the other half of the equation: decision speed. In its fraud management software, GridGain supports 10-20 millisecond machine learning model execution at a minimum of 25,000 transactions per second in an active-active configuration. For A2A leaders, the question is not only how quickly a payment moves, but whether the system can evaluate fraud before the transaction completes.

Figure 2: Financial Analytics Software Company Fraud Model processes sequential model steps until fraud checks are complete.

Together, these examples point to the same conclusion: the organizations best positioned for A2A are the ones that shorten the decision processing window, unify live context, and let legacy and modern systems operate together in an always-on environment.

The path forward

As A2A volumes rise, the real challenge is not simply adding the next rail. It is making sure the architecture stays fast, accurate, and recoverable as real-time demand spreads across the payments estate.

For many teams, the most practical next step is to modernize the transaction layer where approvals, fraud checks, routing, posting context, and recovery have to happen in real time. That reduces risk, improves resilience, and creates a stronger foundation for new rails, higher volumes, and higher customer expectations without forcing a multi-year rip-and-replace program.